2.6 million new jobs were added in 2018 as unemployment dropped to a 40-year low – The Bureau of Labor Statistics reported that U.S. employers added 312,000 new

jobs in December. This shocked analysts that had forecasted 178,000 new jobs.

There were 2.6 million jobs added in 2018, up from 2.2 million new jobs in 2017. The unemployment rate rose to 3.9% from 3.7% in November, a 40-year low, as 419,000 new workers entered the workforce. Optimism about finding an acceptable job and

higher wages were credited with expanding the workforce. Wages rose 3.2% from

one year earlier, matching October’s year over wage gains which marked the largest

year over year wage gain since April 2009.

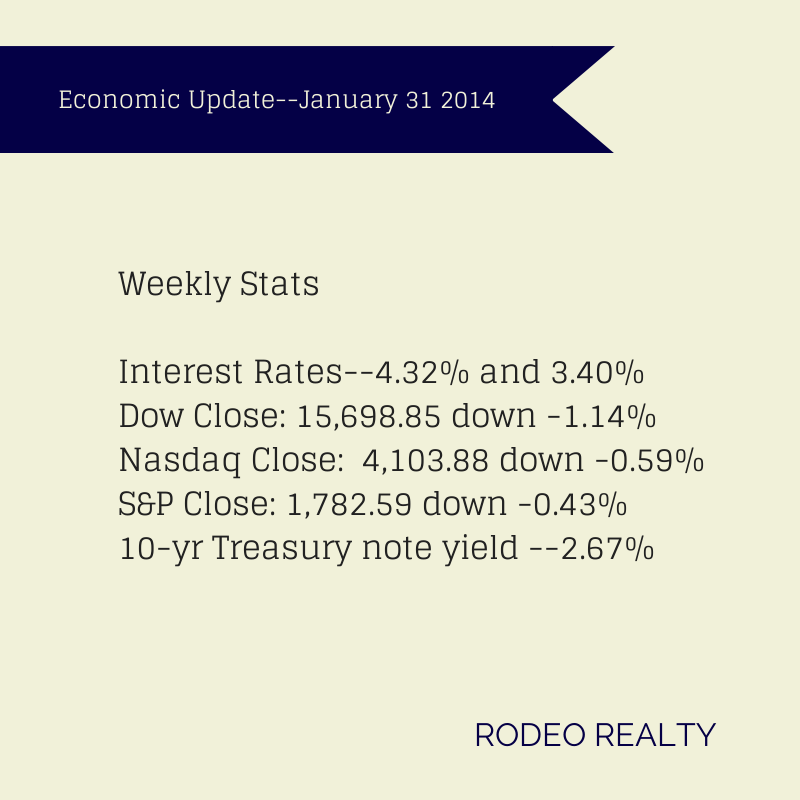

Stock markets ended the year lower in 2018 – After hitting all-time highs in

September, which marked the longest bull market in history, stocks took a downturn in the last quarter of the year. December marked the worst December drop since the Great Depression as fears of a trade war, political uncertainty, slowing economic activity overseas, and higher interest rates made investors more cautious. The Dow Jones Industrial Average ended 2018 at 23,327.46, down from 24,719.22 at the close of 2017.The S&P 500 closed the year at 2,506.85, down from 2,673.51 at the end of 2017. The NASDAQ closed at 6,635.28, down from 6,903.39 on December 31, 2017.

U.S. Treasury Bond Yields higher in 2018 – The 10-year U.S. treasury bond closed the year at a 2.69% yield, up from 2.40% on December 31, 2017. The 30-year treasury yield ended the year at 3.02%, up from 2.74% on December 31, 2017.Mortgage Rates higher in 2018 – The December 28, 2017 Freddie Mac Primary Mortgage Survey reported that the 30 year fixed mortgage rate average was 4.55%, up from 3.99% on December 29, 2017. The 30-year fixed rate was over 5% in October before

declining in November and December. The 15-year fixed was 4.01%, up from 3.44% . last December. The 5-year ARM was 4.00%, up from 3.55% at the close of 2017. Fortunately, rates dropped in the final quarter. The 30-year hit 5% in September.

Year over year price gains moderated in 2018 after 7 years of price gains. For the first 7 months of the year we saw the same month year over year price increases of

6-8%, but by years end those prices were just 1.5% above the same month one year earlier – The California Association of Realtors reported that existing home sales

totaled 372,260 in December on a seasonally adjusted annualized basis. That was

down 11.6% from last December. It marked the fewest sales in a month since January 2015. The statewide median price was $557,600, up 1.4% from December 2017.

On a regional basis Los Angeles County’s median-price of $588,140 was up 1.8%

from last December. Orange County had a median price of $785,000, down 0.1%

from December 2017. Ventura County’s median price of $640,000 was down 0.8% from last December. Inventory levels also continued to rise. Active listings have

increased 30% from 2017. The unsold inventory index hit record lows before moving up steadily in the last 9 months of 2018. There was a3.5-month supply of homes

listed in California, up from a 2.5-month supply in December 2017. It should be noted that a “normal market” has a six-month supply of homes listed, so inventory levels

which are well above the all-time lows of 2017 are still at low historical levels.

Los Angeles County had a 3.5-month supply, up from a 2.4-month supply last

December. Orange County had a 4-month supply, down from 2.6 months last

December. Ventura County had a 5.5-month supply, up from a 4-month supply in

December 2017.