Explore our website for the most up-to-date information on real estate data and local news!

News & Media

Explore our website for the most up-to-date information on real estate data and local news!

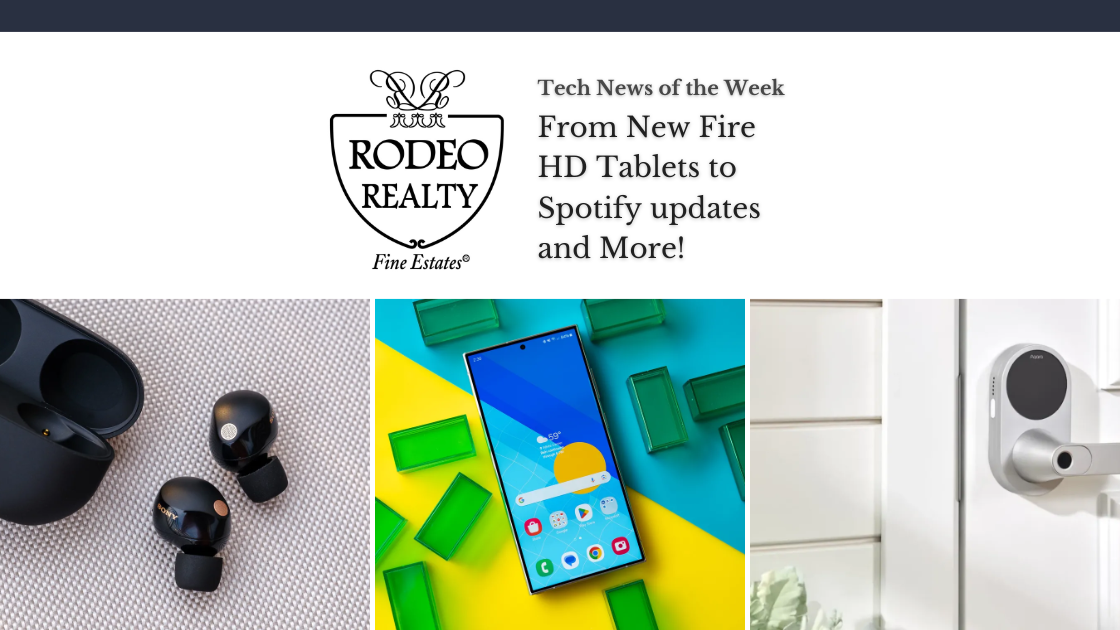

As the week comes to a close, we are rounding out the latest headlines in the world of tech. From New Fire HD Tablets to Spotify updates and more, we have you covered. Check out what’s happening in this week’s blog!

Amazon has unveiled its new Fire HD 8 tablet, featuring generative AI-powered tools like Writing Assist, webpage summaries, and wallpaper creation from prompts. These tools will also be available on other Fire tablets, including the Fire HD 10 and Fire Max 11. The new Fire HD 8 offers improved specs, such as 3GB of RAM, a 5MP rear camera, and up to 13 hours of battery life, with storage options of 32GB or 64GB, expandable via microSD. Priced at $99.99, the new Fire HD is already on sale for $54.99 ahead of Amazon’s Prime Big Deal Days. Rumors suggest upgraded Kindle e-readers may be coming soon.

Sony has released firmware updates for its WF-1000XM5 earbuds and WH-1000XM5 headphones, adding compatibility with Google’s Find My Device network, making them easier to locate if lost. The updates also introduce Auto Switch, a feature from Sony’s new LinkBuds Speaker, allowing seamless playback transition between wireless devices. Users must install Sony’s new Sound Connect app for the updates, which also improve security and streamline Google Fast Pair through LE Audio priority connection for faster pairing with Android devices.

Aqara has introduced its first smart lever lock, the U300, available on Amazon for $229.99. The U300 supports Matter-over-Thread and Apple Home Key, allowing users to unlock doors via apps like Apple Home, Amazon Alexa, and Google Home, as well as using a fingerprint reader, keypad, or physical keys. With weatherproofing, an IPX4 rating, and up to 10 months of battery life, it’s ideal for both interior and exterior doors. The U300 also features a USB-C emergency port and is available in North America, with wider availability expected soon.

Samsung has announced that, starting in 2025, Galaxy device users will be able to tap their phone or smartwatch to unlock smart door locks, similar to Apple’s Home Key feature. By adopting the new Aliro smart lock standard for its Samsung Wallet’s Digital Home Key, Samsung will enable tap-to-unlock and hands-free unlocking for Aliro-compatible locks, utilizing NFC and UWB technology. This feature will allow users to unlock doors without needing to open an app or unlock their phone. The first Aliro-compatible smart locks are expected to hit the market next year.

Spotify has launched a new feature called Offline Backup. The feature automatically generates a playlist of recently streamed songs to keep your music playing when offline. The playlist evolves based on your listening habits. It appears in the app’s home feed whenever an internet connection is lost, provided offline listening is enabled in settings. Available only to premium subscribers, the playlist can be filtered by artist, mood, and genre, and can be permanently added to your library if desired. This feature builds on similar offerings from other streaming services like YouTube Music and Netflix.

Now that October is in full swing, it’s time to get into all the local fun happenings this fall. From festivals to museum exhibits and more, there are plenty of things you can do around town. Check out our weekly round-up!

When: October 6 – July 13, 2024

Where: Academy Museum | Museum Row

What: “Color in Motion” showcases nearly 150 objects, including technology, costumes, props, and film posters, spanning from the 1890s to the present. Divided into six thematic sections, the exhibition explores the relationship between color, music, and movement, as seen in early dance performances and animated shorts. It delves into the evolution of color technologies, from Technicolor and Disney’s women-led Ink & Paint Department to modern digital techniques. The exhibition also highlights monochrome silent films, the narrative significance of color, and experimental art. The final gallery, the Color Arcade, is an interactive, neon-lit space featuring a corridor inspired by the stargate sequence from 2001: A Space Odyssey.

When: October 4 – October 6

Where: South Park

What: While pop culture conventions are plentiful, few local events can match the scale of the annual Los Angeles Comic Con. This massive three-day expo draws thousands of comic fans to Downtown L.A. for a weekend filled with excitement. Attendees can look forward to comic book panels, anime screenings, and celebrity appearances from stars like Ewan McGregor, Hayden Christensen, Rosario Dawson, Michael J. Fox, Christopher Lloyd, Anjelica Huston, Christina Ricci, Giancarlo Esposito, Ming-Na Wen, Lea Thompson, and more. Don’t forget to suit up for the geek couture fashion show and cosplay contest!

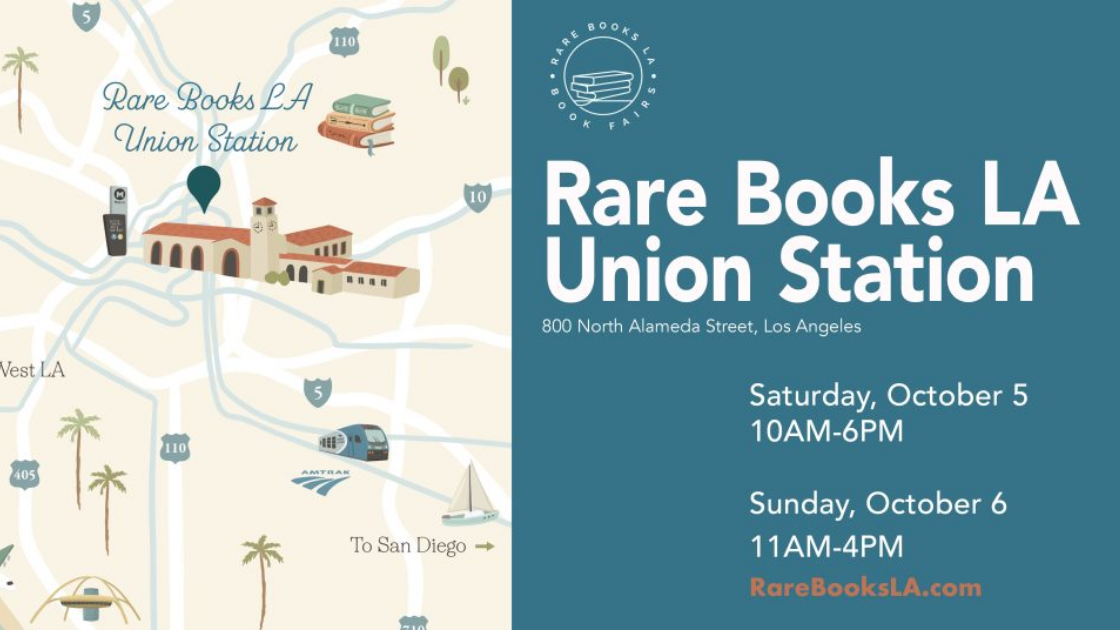

When: October 5 – October 6

Where: DTLA

What: Explore centuries of rare books, prints, photographs, and unique ephemera at this book fair, featuring a curated selection of hard-to-find treasures from dozens of expert dealers.

When: October 5

Where: Westwood

What: One of the city’s most anticipated and mouthwatering fundraising events returns this year, offering bites from some of L.A.’s top restaurants. As you sample dishes from over 60 award-winning chefs, along with selections from renowned wineries, breweries, and bar directors, you’ll also be supporting a great cause—Alex’s Lemonade Stand Foundation, which is dedicated to fighting childhood cancer. For the full lineup of participating chefs, restaurants, bars, wineries, and breweries, click here (just try not to drool—we dare you).

When: October 5

Where: Pacific Palisades

What: Don your wide-brimmed hats and finest Sunday attire for this annual polo match. Enjoy bubbly at this star-studded event, whether from the casual picnic lawn or the exclusive rosé garden. Be sure to arrive early to beat the crowds for the shuttles, which run from nearby school parking lots to Will Rogers State Historic Park, and to grab a drink at the Champagne bars or a bite from the food trucks, which open at 11am. After indulging, make your way to the field to cheer on the teams in the 2pm match.

When: October 4

Where: Culver City

What: Savor crispy tacos while supporting the arts at the Westside’s iconic Tito’s Tacos, as it partners with Tito’s Handmade Vodka to raise funds for the Culver City Arts Foundation. The seventh annual Tito’s Fiesta Mexicana will serve up the restaurant’s beloved tacos, burritos, and flan, along with Tito’s Vodka cocktails. Enjoy five hours of live music, headlined by the Grammy-nominated all-female mariachi band, Mariachi Reyna de Los Angeles.

When: October 4 – November 2

Where: Glendale

What: Step into a Glendale theater (324 N Orange St, Glendale) for a supernatural soirée filled with magic, hauntings, and mystery that will send shivers down your spine. House of Spirits offers a two-hour immersive experience where you can explore eerie performances and macabre pop-ups, all while sipping on themed drinks. Each ticket includes four mini cocktails to accompany your chilling adventure.

When: October 5

Where: North Hollywood

What: The Alvarez family is returning! The cast and executive producers of *One Day at a Time* will reunite for a special charity table read on Saturday, Oct. 5, at 2:00pm at the Saban Media Center in North Hollywood. Fans can look forward to the cast reading unproduced scripts from season four. The event is being produced by former *One Day at a Time* producer Sandi Hochman, along with executive producers Gloria Calderón Kellett, Mike Royce, and Brent Miller.

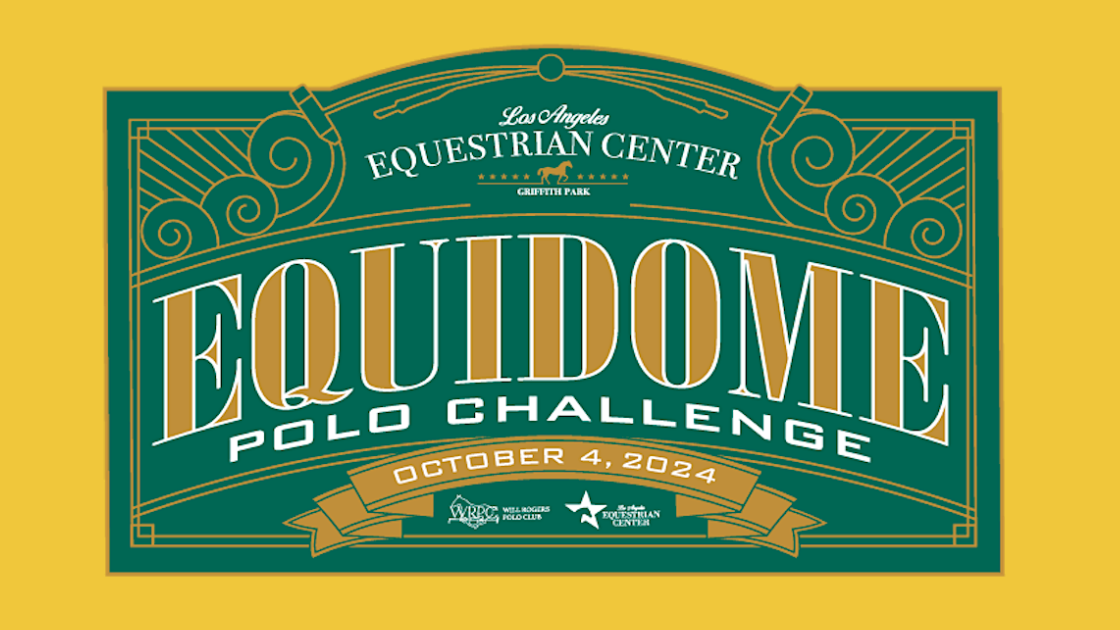

When: October 4

Where: Los Angeles Equestrian Center | 480 Riverside Drive Burbank

What: The October LAEC Equidome Polo Challenge welcomes guests to an evening of fast-paced polo action at the Los Angeles Equestrian Center. Taking place on Friday, October 4, 2024, the event opens its doors at 6:00 PM, with the polo match beginning at 7:00 PM. Spectators will have the chance to witness skilled riders and their majestic horses compete in an exhilarating game of polo. Along with the matches, attendees can enjoy a variety of additional activities, making it a unique opportunity to experience the power, elegance, and athleticism of the sport up close.

When: October 4, 10am – 5pm

Where: Ventura County Fairgrounds

What: The 52nd Annual Harvest Festival® Original Art & Craft Show is set to take place from October 4-6, 2024, at the Ventura County Fairgrounds. This cherished, family-owned tradition returns, bringing together some of the nation’s finest artists and crafters, all excited to present their latest creations. Attendees can look forward to a truly unique shopping experience, featuring one-of-a-kind handmade treasures.

When: October 5, 7:30am – 8:00pm

Where: 60 W Olsen Rd, Thousand Oaks

What: The American Cancer Society Relay For Life of Conejo Valley is a transformative event that unites the community in celebrating cancer survivors, honoring the memories of those lost, and taking action in the fight against cancer. The event aims to raise vital funds and awareness for cancer treatment and research. Likewise, this empowers participants to make a meaningful impact in the battle against the disease.

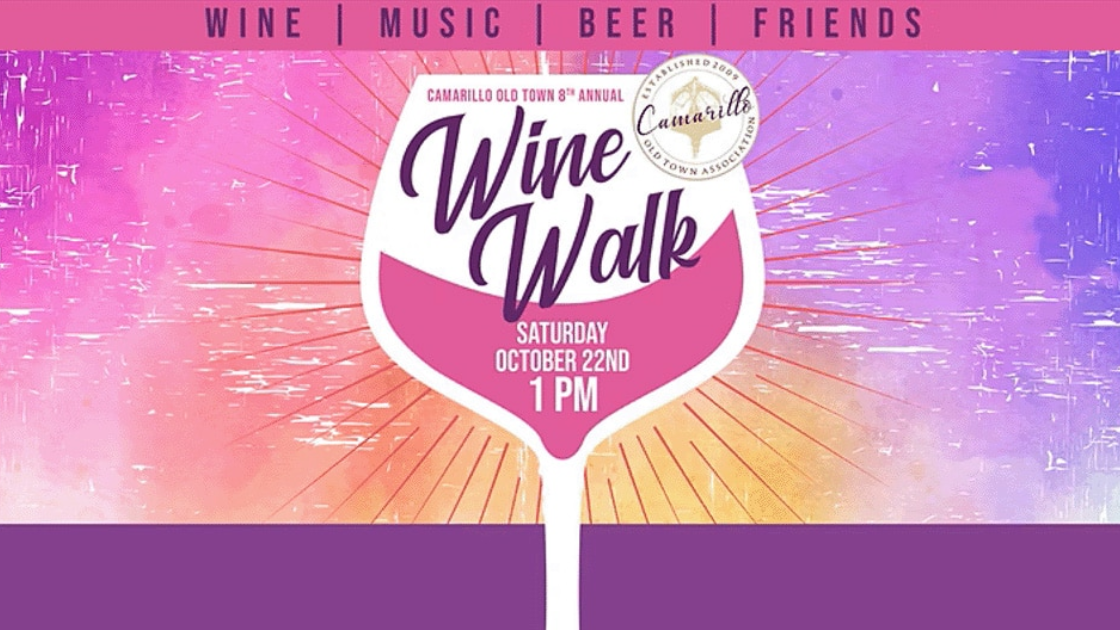

When: October 5, 1pm – 4pm

Where: Old Town, Camarillo

What: Join the 10th Annual Camarillo Old Town Wine Walk on Saturday, October 5, 2024, from 1-4pm, and explore over 20 local businesses along Ventura Blvd, featuring live music and tastings from top regional wineries and craft breweries. Tickets are $55 in advance ($65 at the event, if available) or $75 for the VIP experience. Attendees must be 21+ with valid ID. Proceeds benefit the Camarillo Old Town Association, supporting community events and local retailers. Sign up at www.camarillooldtown.org/10th-annual-wine-walk.

Mooncakes are often imprinted with intricate designs and Chinese characters, symbolizing reunion and prosperity. Traditionally, these pastries are filled with lotus seed paste, red bean paste, and salted duck egg yolks, offering a rich, dense texture. However, mooncakes come in a variety of styles, including Cantonese classics, Taiwanese versions filled with taro or pineapple, and Vietnamese bánh trung thu made with sweetened mung bean, coconut, or even durian. Southern California’s bakeries showcase a wide array of mooncakes. For those seeking a modern twist, you’ll find fillings like chocolate, ice cream, or snow skin-wrapped mooncakes, which appeal to younger generations and adventurous palates. Here are the best spots to find mooncakes in Los Angeles.

Location: 141 N. Atlantic Boulevard, Monterey Park, CA 91754

Aliya Lavaland brings a Thai-Chinese fusion twist to the classic mooncake. Known for their signature lava mooncakes, these pastries feature mung beans and a salted egg yolk center. Another standout is the taro lava mooncake made with coconut milk and taro. If you prefer a non-lava version, they offer flaky-crusted mini mooncakes, and during the Mid-Autumn Festival, they roll out tangerine-shaped mooncakes symbolizing good luck.

Location: 66 E. Montecito Avenue, Sierra Madre, CA 91024

Anita Bakery caters to the health-conscious with two styles of mooncakes: custard and lava custard, both made with salted egg yolks. These Cantonese-style mooncakes are perfect for those seeking a balanced sweet and salty flavor. Anita Chow’s mooncakes are made to order, ensuring fresh, delectable treats for the holiday.

Location: 9430 Warner Avenue, Suite D, Fountain Valley, CA 92708

Vietnamese mooncakes at The Buttery in Fountain Valley stand out for their complexity. The filling is a unique blend of 20 ingredients, including lime leaves, smoked meats, lotus seeds, and a syrup aged for six months. With flavor options like bird’s nest, abalone, and roasted chicken mixed nuts, these savory mooncakes are sure to surprise and delight.

Location: 672 S. Santa Fe Avenue, Los Angeles, CA 90020

Dōmi brings a contemporary take on the traditional dessert with their shortbread crust variations, offering flavors like black sesame, red bean, and jujube. Their moon cookies, a twist on traditional mooncakes with no filling, provide an equally festive and delicious option. Available for pickup in the Arts District or at local farmers markets, Dōmi’s treats are perfect for a modern celebration.

Location: 7609 Garvey Avenue, Rosemead, CA 91770

For those looking for variety, Domie’s Bakery is a mooncake haven, offering over 45 types of mooncakes during the Mid-Autumn Festival. With fillings ranging from traditional white lotus seeds and mixed nuts to taro paste and orange peel with red bean, Domie’s delivers an old-school Cantonese experience.

Locations: Various locations throughout San Gabriel Valley

Kee Wah Bakery brings Hong Kong’s mooncake traditions to SoCal, offering classic fillings like mung bean and white lotus paste alongside contemporary flavors like green tea, chocolate, and caramel sea salt coffee custard. Their beautifully designed packaging, featuring pandas or emperors, makes Kee Wah mooncakes an ideal gift.

Location: 959 N. Broadway, Los Angeles, CA 90012

A Chinatown staple, Kim Hung Bakery offers a wide range of mooncake styles, including Cantonese, Vietnamese, and the flaky-crusted Chiu Chow variety. Fillings range from lotus and winter melon to durian and mung bean, making this spot a go-to for traditionalists and adventurous eaters alike.

Locations: Arcadia, Los Angeles, and Irvine

For a luxurious take on mooncakes, look no further than Lady M. Their limited-edition mooncakes are inspired by the bakery’s famous mille crepe cakes, featuring flavors like Earl Grey, passionfruit, and matcha-chocolate custard. The pastries come in beautifully designed gift sets complete with a lantern and Jade Rabbit projection.

Location: 969 N. Broadway, Los Angeles, CA 90012

Known for its legendary strawberry cakes, Phoenix Bakery also excels in Cantonese-style mooncakes. Whether you prefer red bean, lotus paste, or egg yolks, this 86-year-old bakery has something for everyone. They even offer mini mooncakes for those who want a smaller, more portable treat.

Location: 8450 Valley Boulevard, Rosemead, CA 91770

Royal Bakery specializes in Vietnamese-style mooncakes, offering both baked and snow-skin varieties. These hearty treats feature fillings like mashed mung bean, taro, and mixed nuts, and are best enjoyed with a cup of hot tea.

Locations: Various locations throughout Los Angeles

Taiwanese bakery Sunmerry presents a modern twist with its limited-edition mooncakes. Their flavor lineup includes chocolate, ube milk, milk tea, and mocha coffee from their lava series, as well as Cantonese options with red bean and salted egg yolk. Perfectly packaged, Sunmerry makes for a delightful gift or treat.

Locations: Rowland Heights, Walnut, and Lake Forest

Sunny Dumplings specializes in Shanghainese mooncakes, known for their golden, flaky crusts. Filled with savory pork, these mooncakes offer a flavorful alternative to the sweeter varieties commonly found. Perfect for those who enjoy a savory pastry, they are available at multiple locations across Southern California.

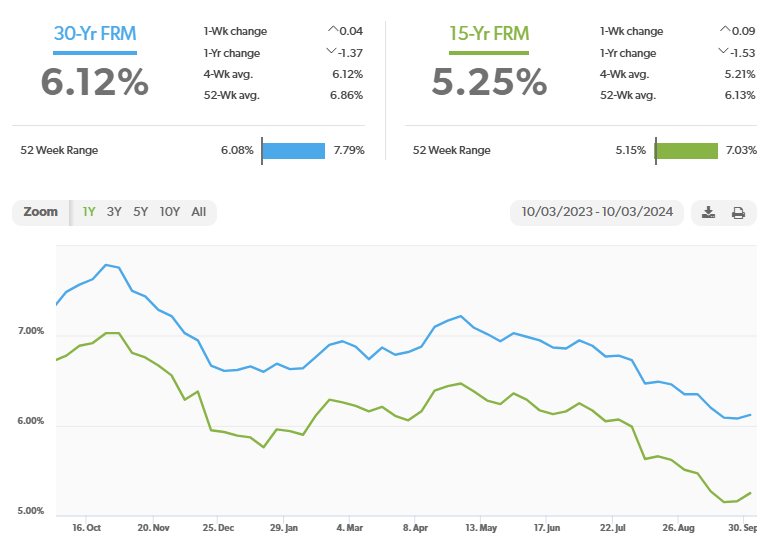

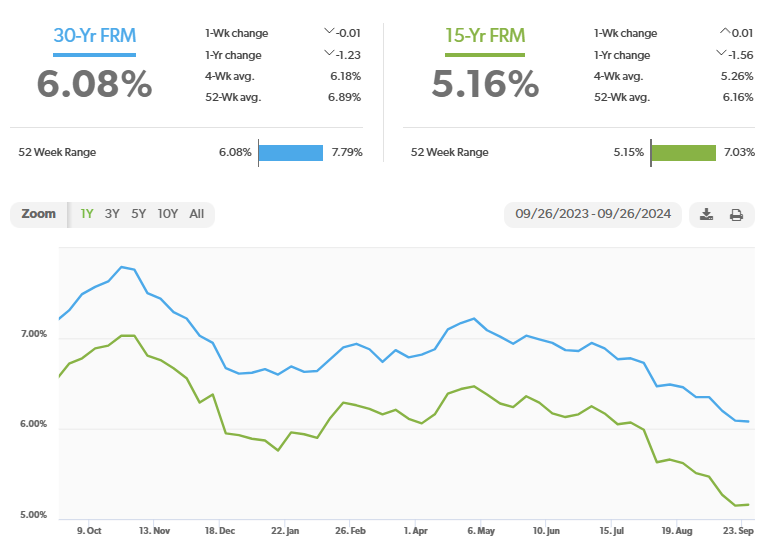

Mortgage rates – Every Thursday Freddie Mac publishes interest rates based on a survey of mortgage lenders throughout the week. The Freddie Mac Primary Mortgage Survey reported that mortgage rates for the most popular loan products as of October 3, 2024, were as follows:

The 30-year fixed mortgage rate was 6.12%, up from 6.08% last week. The 15-year fixed was 5.25%, up from 5.16% last week.

The graph below shows the trajectory of mortgage rates over the past year.

Freddie Mac was chartered by Congress in 1970 to keep money flowing to mortgage lenders in support of homeownership and rental housing. Their mandate is to provide liquidity, stability, and affordability to the U.S.

There are more things to celebrate during the month of October than just Halloween. The tenth month of the year is also a time to celebrate Oktoberfest. Check out all the ways to celebrate in the Los Angeles area below!

When: October 4 – October 26

Every Friday and Saturday in October, the Fairplex transforms into a lively German celebration for Oktoberfest, complete with Bavarian music, beer, and the famous chicken dance. Feast on bratwurst, knockwurst, and sweet corn while enjoying authentic German beers at this 21+ event. The party atmosphere is enhanced by DJs, oompah bands, and the Das Kär Show, showcasing over 40 Volkswagen Beetles and other German-made cars. For those looking to double their fun, a “Boos & Brews” combo ticket is available for $30, offering entry to both Oktoberfest and Lights Out, the Fairplex’s other October attraction.

When: Until October 26

Starting on September 28, Wurstküche Venice kicks off three weekends of Bavarian festivities, including live music, lederhosen, and mouth-watering bites. Savor their unique rattlesnake and rabbit sausage topped with onions and peppers, and pair it with a variety of German and Belgian beers on draft. Yodeling and traditional German tunes create a fun, lively atmosphere. Each $50 ticket includes a signature Wurstküche beer mug and your first fill-up, with Saturday and Sunday start times offering multiple chances to join the celebration.

When: Until November 3

Touted as “Orange County’s biggest party since 1977,” Old World Oktoberfest offers a Bavarian-inspired experience with ocean views. From September 8 through November 3, the festivities include “Shot Girls,” dancers, and live oompah bands every Wednesday to Sunday. The famous wiener dog races make a comeback at the kickoff event, with additional races scheduled throughout the season. While Friday and Saturday nights are reserved for the 21+ crowd (with a cover charge), families can join the fun on Saturday afternoons and select evenings, with free entry on Wednesdays and Thursdays.

When: Until November 2

Escape to the mountains for Big Bear Lake’s annual Oktoberfest, running every weekend from September to early November. Enjoy authentic German beer, hearty knockwursts, and festive attire as the party unfolds. The event features multiple live bands, including four flown in from Germany, and plenty of entertainment. Don’t miss the stein-carrying contest, where one lucky participant will be crowned Oktoberfest Queen.

When: October 4

Swap pretzels for dumplings at San Gabriel’s Dumpling & Beer Fest, held at the Mission Playhouse on October 4. Your entry includes a beer tasting wristband, giving you unlimited access to craft brews from 6 to 10 p.m. Satisfy your cravings with dumplings from various food trucks, while live DJs keep the party going all night. Families can enjoy arts and crafts stations for kids, making this a fun event for all ages.

When: October 12-20, 2024

Santa Anita Park combines horse racing with Oktoberfest fun over two weekends in October. Get in on the action with stein-holding contests, costume competitions, and plenty of beer and pretzels. Each $38 general admission ticket includes a mini stein and eight beer tastings, along with a $5 betting voucher, tip sheet, and access to grandstand seating. Opt for the $75 VIP group ticket for reserved picnic table seating and a $20 food voucher.

When: September 14 – October 27

Nestled in the “Alps of Southern California,” Lake Arrowhead’s Oktoberfest runs every weekend through October 27. The event features live German-American oompah bands, stein-holding contests, children’s games, and a daily sausage toss competition. Although there’s no entry fee, attendees can book picnic or pub tables for up-close views of the stage, with prices starting at $25 for Sunday reservations.

When: October 5

On October 5, the Rose Bowl hosts CraftoberFest, an Oktoberfest-inspired event showcasing over 50 local craft breweries. This all-ages celebration offers unlimited craft beer and kombucha tastings with the purchase of a ticket, along with traditional Bavarian food like pretzels and bratwurst. Enjoy live music from Festmeister Hans and Die Sauerkrauts as you dance the day away. Upgrade to VIP for early entry and exclusive seating.

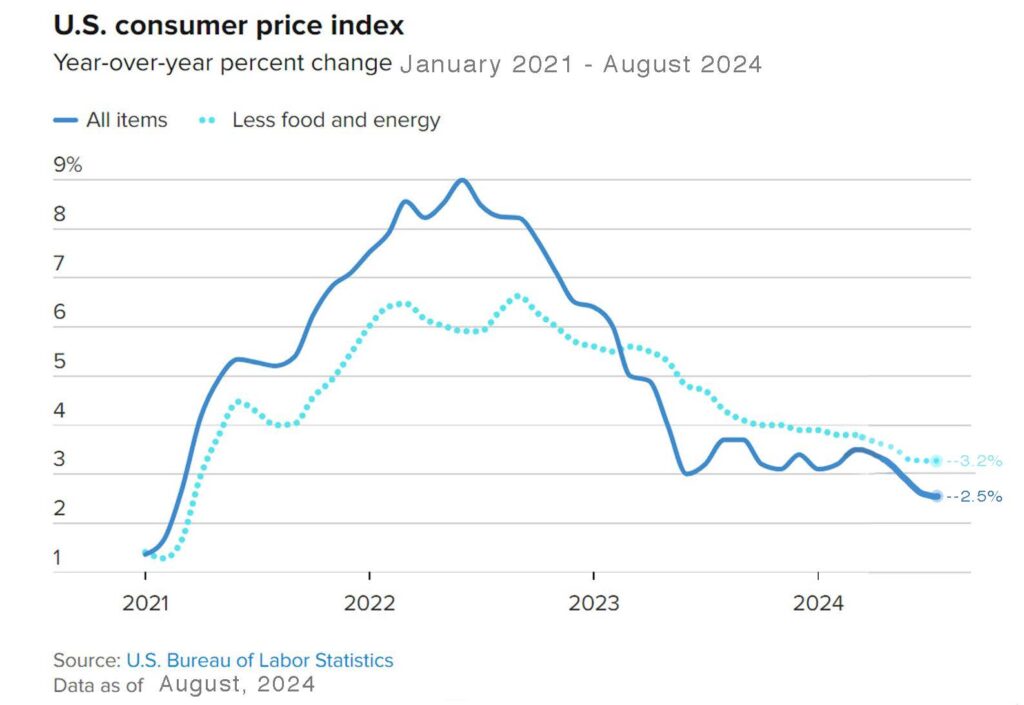

Federal Reserve declares that inflation is under control and makes its first rate cut in four years – The Fed dropped its key interest rates by a ½% in September. With inflation spiking in 2022, the Fed enacted one of its most aggressive rate hike campaigns in history. They increased rates steadily until they hit a 25-year high. Now that inflation has worked its way down the Fed has begun a campaign of dropping rates to a more “neutral rate” from their previous “restrictive rate.” Experts expect two more rate drops before the end of the year, likely .25% each. The inflation reports for August were as follows: The Consumer Price Index (CPI) measured 2.5% in August. It peaked at 9.1% in June 2022 and has worked its way down slowly over the past twenty-eight months. The Producer Price Index (PPI) showed wholesale rose just 1.7% from last August. The Personal Consumption Expenditure Index (PCE) for August, a key gauge of inflation that the Fed focuses on to measure the cost of goods and services in the U.S. economy showed that the 12-month inflation rate was 2.2%, down from 2.5% in July and its lowest reading since February 2021. On Friday we will get the September Jobs report. That report will have an impact on bond yields and mortgage rates, which did not drop after the Fed announced its rate drop. That drop was expected and was already “built into” long-term bond yields and mortgage rates. The government released its third revision of the second quarter Gross Domestic Product (GDP), the broadest measure of the strength of the economy. It showed that the economy grew at a 3% annualized pace in the second quarter, a faster rate than Wall Street had expected. The Fed is pointing to a “soft landing” where they expect the economy to remain healthy while inflation continues to moderate. Many experts felt that the dramatic rise in rates would put the country into a recession but so far that has not happened. With the Fed now lowering rates the hope is that a recession will be avoided.

The graph below shows the movement of the Consumer Price Index from 2021 to the present.

Stock Markets – The Dow and S&P 500 closed September at record highs, and the NASDAQ closed just 2.5% off its record set in July. The Dow Jones Industrial Average closed the month at 42,330.15, up 1.8% from 41,563.08, on August 31, 2024. It is up 12.3% year-to-date. The S&P 500 closed the month at 5,762.58, up 2% from 5,648.40 last month. It is up 20.8% year-to-date. The NASDAQ closed the month at 18,189.17, up 2.7% from 17,713.63 last month. It is up 21.2% year-to-date.

U.S. Treasury bond yields – The 10-year treasury bond closed the month yielding 3.81%, down from 3.91% last month. The 30-year treasury bond yield ended the month at 4.14%, down from 4.20% last month. We watch bond yields because mortgage rates often follow treasury bond yields.

Mortgage rates – Every Thursday Freddie Mac publishes interest rates based on a survey of mortgage lenders throughout the week. The Freddie Mac Primary Mortgage Survey reported that mortgage rates for the most popular loan products as of September 26th, 2024, were as follows: The 30-year fixed mortgage rate was 6.08%, down from 6.35% at the end of August. The 15-year fixed was 5.16%, down from 5.51% last month.

The graph below shows the trajectory of mortgage rates over the past year.

Freddie Mac was chartered by Congress in 1970 to keep money flowing to mortgage lenders in support of homeownership and rental housing. Their mandate is to provide liquidity, stability, and affordability to the U.S.

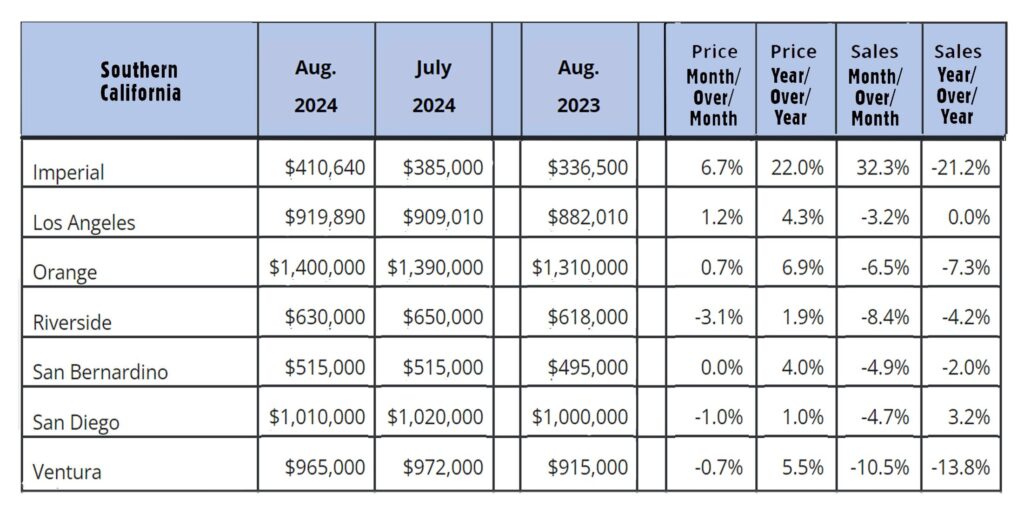

Home sales data was released on the third week of the month for the previous month by the National Association of Realtors and the California Association of Realtors. These are August’s home sales figures.

U.S. existing-home sales August 2024 – The National Association of Realtors reported that existing-home sales totaled 3.86 million units on a seasonally adjusted annualized rate in August, down 4.2% from an annualized rate of 4.03 million last August. The median price for a home in the U.S. in August was $416,700, up 3.1% from $404,200 one year ago. There was a 4.2-month supply of homes for sale in August, up from a 3.3-month supply one year ago. First-time buyers accounted for 26% of all sales. Investors and second-home purchases accounted for 19% of all sales. All cash purchases accounted for 26% of all sales. Foreclosures and short sales accounted for 1% of all sales.

August California existing-home sales report – The California Association of Realtors reported that existing-home sales totaled 262,050 on an annualized rate in August, up 2.8% from a revised 254,820 homes sold on an annualized basis last August. The statewide median price paid for a home in July was $888,740, up 3.4% from $859,670. one year ago. There was a 3.2-month supply of homes for sale, up from a 2.4-month supply in August 2023.

The graph below lists home sales data by county in Southern California.

Clutter has a way of sneaking up on us. One day your space is tidy, and the next, random mason jars have found a home on your microwave. But decluttering doesn’t have to be overwhelming. With just a few easy steps, you can bring order back to your home. Check out our blog for the best tips on clearing the clutter and keeping your space organized!

No matter what type of container you use, make sure it’s a sturdy one. Having containers you can carry easily helps in maintaining easy organization.

One of the biggest motivators for decluttering is to keep your giveaway bin nearby as you work. Placing it in the area, you are decluttering keeps everything easily accessible for its final removal from your house.

If you make the decision on the final destination of your clutter before you start placing it in the container, it will make the process of selection much easier. When you make a large pile of stuff before knowing what you’ll do with it, it can take away any motivation you may have had before you got started.

Instead of trying to declutter your entire home in a single, exhausting shot, try doing it for two or three 15-minute periods over the span of several days. This will help you prevent exhaustion and anxiety, which can lead to you losing your motivation. Once you are finished, you can continue creating a habit of decluttering for 10 minutes a day. In the end, you will have not only cleaned your home of clutter, but you have made sure it never accumulates again!

5. Get Rid Of Clutter While You Are Doing Other Things

5. Get Rid Of Clutter While You Are Doing Other ThingsYou can use those few minutes while you are doing something else to de-clutter certain parts of your home. For example, if you are waiting for a pot of soup to cook, you can make use of the time it takes to get rid of the clutter in your kitchen drawer. Multitasking is probably one of the best ways to keep things organized throughout the household.

As you declutter your home, it’s essential to get rid of the items as soon as you have a full box. Before moving another one next to it, get rid of the full one quickly. This means taking it to its final destination before you end up with a pile of clutter boxes next to your door.

| Economic news for the week – The August Personal Consumption Expenditure Index (PCE), a key gauge the Fed uses to evaluate U.S. goods and services costs, was released. It showed that the 12-month inflation rate was 2.2%, down from 2.5% in July and its lowest reading since February 2021. The Bureau of Economic Analysis released its third revision of the second quarter Gross Domestic Product (GDP), the broadest measure of the strength of the economy. It showed that the economy grew at a 3% annualized pace in the second quarter, a faster rate than Wall Street had expected. These reports were another indicator that the Fed may be correct in their expectations of a “soft landing,” where inflation comes under control and the economy remains strong. We are seeing investors feeling optimistic as well. They pushed stock markets higher again this week. Stock markets have closed higher in six of the last seven weeks. All indexes hit record highs this week with the Dow closing the week at an all-time high and the Nasdaq and S&P 500 closing just off their highs set earlier in the week. It appears that investors are very optimistic about the prospects of lower interest rates and the strength of the economy.

Stock markets – The Dow Jones Industrial Average closed the week at 42,313.00, up 0.6% from 42,063.36 last week. It is up 12.3% year-to-date. The S&P 500 closed the week at 5,738.18, up 0.6% from 5,702.55 last week. The S&P is up 20.3% year-to-date. The Nasdaq closed the week at 18,119.59, up 1% from 17,948.32 last week. It is up 20.7% year-to-date. U.S. Treasury bond yields are slightly up this week – The 10-year treasury bond closed the week yielding 3.75%, up slightly from 3.73% last week. The 30-year treasury bond yield ended the week at 4.10%, up slightly from 4.07% last week. We watch bond yields because mortgage rates follow bond yields. Mortgage rates – Every Thursday Freddie Mac publishes interest rates based on a survey of mortgage lenders throughout the week. The Freddie Mac Primary Mortgage Survey reported that mortgage rates for the most popular loan products as of September 26, 2024, were as follows: The 30-year fixed mortgage rate was 6.08%, almost unchanged from 6.09% last week. The 15-year fixed was 5.16%, almost unchanged from 5.15% last week. The graph below shows the trajectory of mortgage rates over the past year.

Freddie Mac was chartered by Congress in 1970 to keep money flowing to mortgage lenders in support of homeownership and rental housing. Their mandate is to provide liquidity, stability, and affordability to the U.S. Have a great weekend! |

Stay connected with this week‘s top headlines in the world of tech! From Meta’s AR Glasses to a New Leica and more, we have you covered. Check out the latest news below!

Leica shakes up its Q series with the launch of the Q3 43, featuring a 43mm f/2 lens for tighter shots and portraits. This new Leica variant retains the same 60-megapixel sensor and features as the standard Q3 but offers a fresh aspherical APO-Summicron lens for $6,895. Though nearly identical in specs, the Leica Q3 43 distinguishes itself with a gray leatherette and digital cropping options up to 150mm. Despite the premium price, Leica disappoints by omitting the battery charger, making it an optional $200 accessory. Still, the Leica 43mm lens offers a fresh appeal for fans wanting a more versatile field of view.

![]()

Just like fashion trends, tech gadgets are making a style comeback. After the ’80s beige keyboards and ‘90s gray video game consoles, transparent gadgets from the early 2000s, like see-through iMacs and N64 controllers, are re-emerging as the next big trend. Today, we see clear smartphones like the Nothing Phone, transparent Beats Studio earbuds, and colorful translucent gaming consoles making waves. As transparent tech reclaims the spotlight, it’s a perfect time to revisit those classic see-through devices from the past.

Meta’s first augmented reality glasses, Orion, represent CEO Mark Zuckerberg’s vision for post-smartphone technology. While the glasses showcase cutting-edge features like a 43mm field of view, Micro LED projectors, and AI capabilities, the device is too costly and complex to mass-produce at $10,000 per unit. With silicon carbide lenses and a neural wristband for gesture control, Orion delivers an immersive AR experience, but it’s still far from ready for consumers, serving primarily as a prototype for future AR innovations.

California Governor Gavin Newsom signed the Phone-Free School Act, requiring all schools statewide to limit cellphone use by July 2026. The law aims to reduce smartphone-related mental health issues in students, with exceptions for emergencies and certain permissions. Schools must create policies promoting responsible smartphone use while supporting student well-being. Despite opposition from the California School Boards Association, the law is part of a growing trend, with at least 15 states already implementing similar restrictions.

Raycast, a powerful Mac tool known for its advanced app launcher and multitasking capabilities, is expanding to Windows and iOS. Initially built as a faster alternative to Apple’s Spotlight, Raycast now allows users to manage apps, windows, and even chat with AI. Co-founder Thomas Paul Mann announced plans to release the Windows version, which may offer even more control, next year. The iOS app will be a simplified companion tool. Alongside the expansion, Raycast raised $30 million to further reduce busywork and streamline productivity with AI integration.