| Stock markets closed higher for the third consecutive week – Stock markets closed higher again this week capping off a third week of gains following a tough October. The October Consumer Price Index (CPI) was released this week. It showed that consumer prices in October had climbed 3.2% from one year earlier. While the Fed target is 2%, this was a giant step in the right direction. Inflation peaked in June 2022 at 9.1% and worked its way down every month for a year hitting 3% in June. In July, August, and September the year-over-year inflation rate worked its way back up. It was 3.7% in September, so dropping to 3.2% in October was welcome news to investors. The Producer Price Index showed inflation taming as well in October. Bond yields and mortgage rates have fallen steadily in November on this news and many experts feel that rising inflation, higher interest rates, and Fed hikes are behind us. The Dow Jones Industrial Average closed the week at 34,947.28, up 1.9% from 34,283.10 last week. It is up 5.4% year-to-date. The S&P 500 closed the week at 4,514.02, up 2.2% from 4,415.24 last week. It is up 17.6% year-to-date. The Nasdaq closed the week at 14,125.48, up 2.4% from 13,798.11 last week. It is up 35% year-to-date.

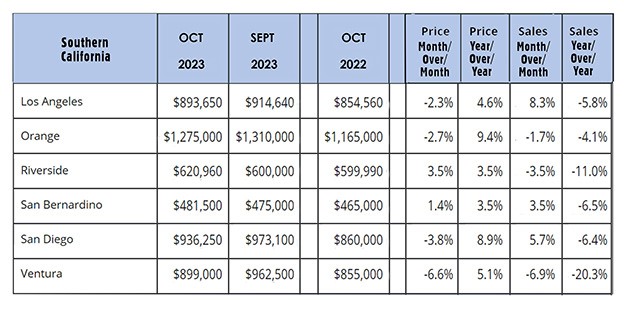

U.S. Treasury bond yields – The 10-year treasury bond closed the week yielding 4.44%, down from 4.61% last week. The 30-year treasury bond yield ended the week at 4.59%, down from 4.73% last week. We watch bond yields because mortgage rates follow bond yields. Mortgage rates – The Freddie Mac Primary Mortgage Survey reported that mortgage rates for the most popular loan products as of November 9, 2023, were as follows: The 30-year fixed mortgage rate was 7.44%, down from 7.50% last week. The 15-year fixed was 6.76%, down from 6.81% last week. Rates dropped all week. California existing-home sales – The California Association of Realtors reported that existing-home sales totaled 241,710 units on a seasonally adjusted annualized basis in October, down 11.9% from a revised 274,410 annualized sales pace in October 2022. October marked the thirteenth straight month of the annualized sales rate dropping under 300,000 on an annualized basis, and the second consecutive month of sales dropping below 250,000 annualized sales, a level that was thought could never happen. Year-to-date, the number of homes sold were down 27.2% in October. The statewide median price paid for a home in October was $840,360, up 5.3% from a revised $798,140 a year ago. There was a 2.7-month supply of homes for sale in October, down from a 3.1-month supply one year ago. The graph below shows sales data by county in Southern California.

|

Economic Update | Week Ending November 18, 2023