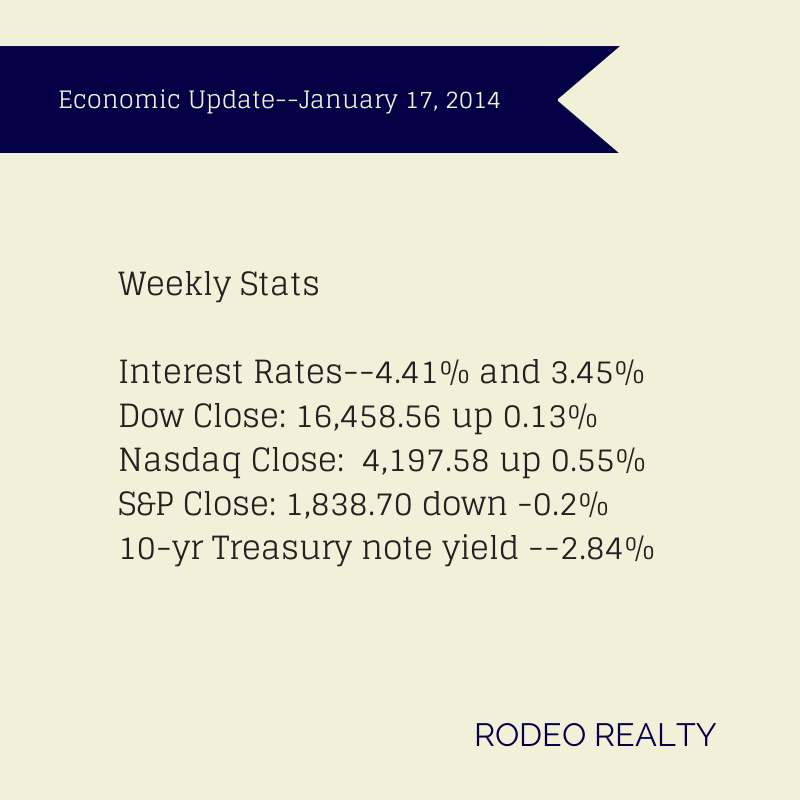

Stocks did a little consolidating this week as investors digested the jobs numbers and continued to ponder the strength of the economic recovery. The Dow and Nasdaq were up for the week but the S&P was slightly lower. The Dow closed out the week at 16,458.56 up 0.13% from last week’s close of 16,437.05. The Nasdaq closed at 4,197.58 up 0.55% from last week’s 4,174.66 close. The S&P 500 finished the week at 1,838.70 down –0.2% from last week’s 1,842.37 close.

Stocks did a little consolidating this week as investors digested the jobs numbers and continued to ponder the strength of the economic recovery. The Dow and Nasdaq were up for the week but the S&P was slightly lower. The Dow closed out the week at 16,458.56 up 0.13% from last week’s close of 16,437.05. The Nasdaq closed at 4,197.58 up 0.55% from last week’s 4,174.66 close. The S&P 500 finished the week at 1,838.70 down –0.2% from last week’s 1,842.37 close.

On the heels of last week’s low job creation numbers there is some positive employment news, The U.S. Department of Labor reported that the number of job openings in November hit 4 million, up more than 5% from a year before and the highest level since March 2008. The number of quits rose to 2.43 million, the most since September 2008, showing that many workers are seeing more prospects out there and are willing to change jobs.

The latest survey on consumer sentiment fell in January with a reading of 80.4 as compared to a reading of 82.5 in December, well below economists’ forecasts of an 84 reading. Survey respondents may have been reacting to the recent job numbers as well as a slight uptick in the average price of gasoline (up to an average of $3.296 per gallon compared to last month’s $3.216 per gallon).

U.S. housing starts fell less than expected in December. The Commerce Department reported that groundbreaking fell -9.8% to a seasonally-adjusted rate of a 999,000-unit pace, the largest percentage decline since April but above economists’ expectations of a 990,000-unit rate in December. For all of 2013, housing starts rose 18.3% to an average of 923,400-unit rate. Groundbreaking for single-family homes fell 7% to a 667,000-unit pace in December while the multifamily homes segment declined 14.9% to a 332,000-unit rate. Permits to build homes fell 3% in December to a 986,000-unit pace but for all of 2013, permits increased 17.5% to an average of 974,700-units.

The 10-year Treasury note yield rate remained relatively steady this week ending at 2.84%, after last week’s 2.88% close. It was 1.89% a year ago.

Interest rates dropped this week awaiting the next meeting of the Fed later this month. The Freddie Mac Weekly Primary Mortgage Market Survey showed that the 30-year-fixed rate dropped to 4.41% from 4.51% last week. The 15-year-fixed fell to 3.45% from last week’s 3.56%. A year ago the 30-year fixed was at 3.38% and the 15-year was at 2.66%.

The California Association of Realtors® (C.A.R.) released numbers showing that California home sales fell for the fifth straight month in December partly because the distressed market plays a smaller role in the state’s housing market so there was less movement by lenders trying to move properties off their books by the end of the year. Closed escrow sales of existing, single-family detached homes in California totaled a seasonally adjusted annualized rate of 361,890 units in December, down -6.7% from a revised 387,860 in November and down -18.6% from a revised 444,770 in December 2012. For 2013 as a whole, a preliminary 413,870 single-family homes closed escrow in California, –5.9% from a revised 2012 figure of 439,790.

Home prices rose in December according to C.A.R. The statewide median price of an existing, single-family detached home rose 3.7% from November’s median price of $422,210 to $438,040 in December. December’s price was 19.7% higher than the revised $365,840 recorded in December 2012, marking a year and a half of double-digit annual gains and the first time in 15 months that the annual increase was below 20%. For Los Angeles County the median sold price $439,590 was up 8.5% over November’s $405,260 price and up 19.6% over December 2012’s $367,400 price. The amount of sales was up 9.5% month over month but down -15.1% year over year. The available supply of existing, single-family detached homes for sale dropped in December to 3 months, down from November’s Unsold Inventory Index of 3.6 months, it was 2.6 months in December 2012. The median number of days it took to sell a single-family home also increased to 40.2 days in December, up from 36.7 days in November and from 38.1 days in December 2012.

The latest information from DataQuick shows that home sales across the six-county Southland area fell to a six-year-low for December while the median price paid for a home rose to the highest level in nearly six years. A total of 18,415 homes were sold in Los Angeles, Riverside, San Diego, Orange, Ventura, and San Bernandino counties last month. The number was up 6.5% from 17,283 sales in November and down -9.2% from 20,274 sales in December 2012. Last month’s sales were -24.1% lower than the average number of sales in the month of December. The median sales price for the Southland region was $395,000 last month 2.6% gain from November and 22.3% over December 2012. DataQuick attributes the numbers to investor activity decreasing as buyers faced a low inventory of homes with demand continuing to outstrip supply. The typical monthly mortgage payment Southland buyers committed themselves to paying last month was $1,594, up from $1,517 the month before and up from $1,139 a year earlier. Buyers paying cash in December accounted for 27.7% of home sales, down from 28.0% the month before and down from 35.8% a year earlier. For Los Angeles County alone 7,198 homes were sold compared to 6,240 last December, a decrease of -13.30%. The median price in LA Country rose year over year from $352,000 to $430,000, a gain of 22.2%.

CoreLogic reported that the number of completed foreclosures and the U.S. foreclosure inventory were down in November. There were 46,000 completed foreclosures in the United States in November 2013, down -29% from 64,000 in November 2012. Month over month foreclosures were down 8.3% from 50,000 in October. Before the housing crash, completed foreclosures averaged 21,000 per month (2000 to 2006). The total U.S. foreclosure inventory dropped 34% with 812,000 homes in some stage of foreclosure in November, compared to 1.2 million in November 2012. Foreclosure inventory represented 2.1% of all homes with a mortgage, compared to 3% in November 2012. The rate of seriously delinquent mortgages is at its lowest level since November 2008.

Realty Trac reported that foreclosure activity dropped by -26% in 2013 and U.S. homes that got started on the path to foreclosure fell last year to a low not seen since before the housing boom. Foreclosure starts were down 33% from a year earlier and at the lowest annual level since 2006.

The National Association of Home Builders released their latest survey which shows builder confidence holding relatively steady. The NAHB/Wells Fargo Housing Market Index was at 56 points in January from a downwardly revised 57 in December. The December reading originally reported at 58 was the highest level since August. Rising prices, low interest rates and continued demand continue to make home builders optimistic about the current market.

The Consumer Price Index increased 0.3% in December, the largest 1-month increase since June 2013 however much of that was due to energy prices. Year-over-year prices rose 1.5%, well under the Federal Reserve’s 2% inflation target.

very active. We are starting to see the beginning of another price surge!