This week marked an unusual amount of economic news and reports.

U.S. economy posts robust growth in second quarter – The Gross Domestic Product (GDP) for the second quarter increased at an annual rate of 3% according to the US Bureau of Economic Analysis. This was a tremendous turnaround from a 0.5% drop in the first quarter of the year.

Fed’s favorite gauge of inflation shows inflation heated up in June – The Personal Consumption Expenditure Index (PCE), the Fed’s preferred index for gauging inflation, jumped 2.6% at an annual rate in June, up from 2.4% in May. That marked the highest inflation level since February and more importantly a sign that inflation, which has steadily decreased since peaking in 2022 is beginning to rise.

Federal Reserve leaves interest rates unchanged – The Fed met this week and decided to leave interest rates unchanged. President Trump has been criticizing Fed Chairman Powell for not lowering rates now that inflation is closer to the Fed’s 2% target rate after peaking at 9% in 2022. Powell has cited inflation potential due to tariffs as the Fed’s reluctance to lower rates.

U.S. job growth stalled in July – The Bureau of Labor and Statistics reported that 73,000 new jobs were added in July. That was far below the number of jobs that analysts had forecasted, suggesting that the job market may finally be showing signs of stalling. The unemployment rate increased slightly to 4.2%, up from 4.1% in June. The hiring numbers for May and June were also revised sharply lower. The revised figures brought the number of new jobs down in those two months by 258,000, a huge reduction from the initial figures reported. May was revised from 125,000 new jobs to 19,000, and June was revised from 14,000. This took everyone by surprise. Following the release, President Trump abruptly fired the commissioner of the Bureau of Labor Statistics, stating that she manipulated the monthly jobs report for political purposes.

Stock Markets – Stock markets dropped sharply this week on fears that hiring had slowed and that tariffs were beginning to stall growth. The Dow Jones had its worst week since April, and the S&P had its worst week since May 23, snapping 6 consecutive weeks of gains and record highs. The Dow Jones Industrial Average closed the week at 43,588.58, down 2.9% from 44,901.92 last week. Year-to-date, it is down 2.1% from 44,544.66 on December 31, 2024. The S&P 500 closed the week at 6,238.01, down 2.4% from 6,388.64 last week. Year-to-date, the S&P is up 3.3% from 6,040.53 on December 31, 2024. The Nasdaq closed the week at 20,650.13, down 2.2% from 21,108.32 last week. Year-to-date it is up 5.2% from 19,627.44 on December 31, 2024.

U.S. Treasury bond yields – The 10-year treasury bond closed the week yielding 4.23%, down from 4.40% last week. The 30-year treasury bond yield ended the week at 4.81%, down from 4.92% last week. We watch bond yields because mortgage rates follow bond yields

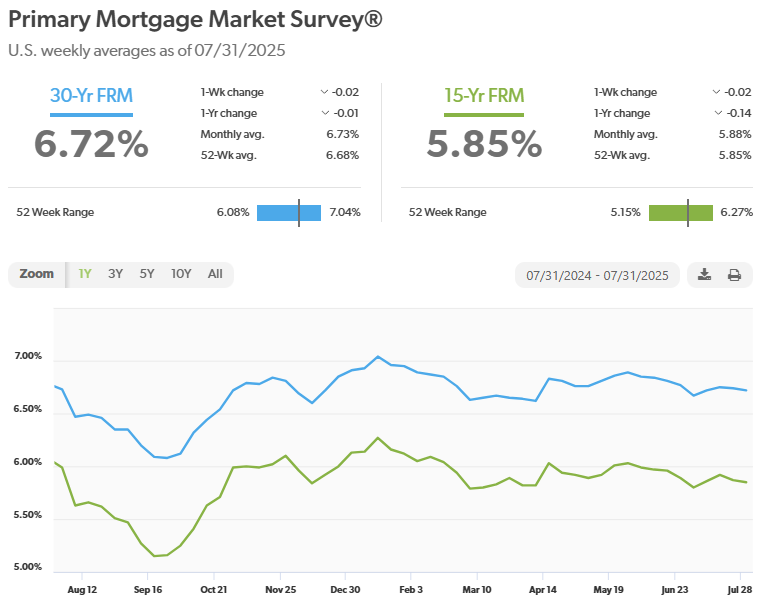

Mortgage rates – Every Thursday Freddie Mac publishes interest rates based on a survey of mortgage lenders throughout the week. The Freddie Mac Primary Mortgage Survey reported that mortgage rates for the most popular loan products as of July 31, 2025, were as follows: The 30-year fixed mortgage rate was 6.72%, nearly unchanged from 6.74% last week. The 15-year fixed was 5.85%, nearly unchanged from 5.87% last week.

The graph below shows the trajectory of mortgage rates over the past year.

Have a Great Weekend!

Have a Great Weekend!