| It was a wild first week of the year. It began with US military action in Venezuela with the promise of returning US oil companies to run oil production, in what is believed to be the largest reserves of oil in the world. Followed by an announcement by President Trump to purchase mortgage securities to drop long-term interest rates, an estimate of fourth-quarter GDP that was off the charts, and a mixed December jobs report. This all caused stocks to surge to record highs.

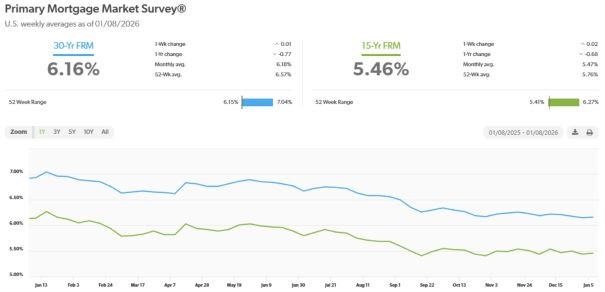

Housing & Mortgage Rates: President Trump announced a plan directing Fannie Mae and Freddie Mac to purchase $200 billion in mortgage-backed securities, a move aimed at putting downward pressure on mortgage rates and improving affordability. The idea is to help offset the Federal Reserve’s ongoing pullback from the mortgage market and narrow the spread between mortgage rates and Treasury yields. Still, the announcement has been viewed positively by markets as a signal of increased policy support for housing. We saw 30-year mortgage rates drip to under 6% on Friday after Thursday’s announcement, the lowest rate since 2022. Mortgage rates – Every Thursday, Freddie Mac publishes interest rates based on a survey of mortgage lenders throughout the week. The Freddie Mac Primary Mortgage Survey reported that mortgage rates for the most popular loan products as of January 8, 2026, were as follows: The 30-year fixed mortgage rate was 6.16%, nearly unchanged from 6.15% last week. The 15-year fixed was 5.46%, nearly unchanged from 5.44% last week. If Friday’s rates hold, we will see a big dip in next week’s survey rates. The graph below shows the trajectory of mortgage rates over the past year.

December Jobs report shows hiring was sluggish while the unemployment rate dipped – Recent labor market data point to a continued moderation in U.S. hiring activity. The Bureau of Labor Statistics reported that 50,000 new jobs were added in December. That was below analyst’s expectations of 70,000. Revisions to the prior two months reduced reported job gains by a combined 76,000. As a result, average monthly job growth for 2025 stands at 49,000, down from 168,000 in 2024, and the three-month average has turned modestly negative. For the year employers added just 584,000 jabs last year, down from 2.2 million new jobs in 2024, marking its worst non-recession year of job growth since 2003. At the same time, the unemployment rate dropped to 4.4% in December, down from a revised 4.5% in November. That is better than economists’ expectations of 4.5% and below the long-term historical average of approximately 5.5%. Despite the slowdown in hiring, average hourly earnings rose 3.8% compared to one year ago. Estimated 4th quarter U.S. GDP suggest a surge in output – The Federal Reserve Bank of Atlanta’s GDPNow model sharply revised its estimate for U.S. fourth-quarter GDP growth to 5.4% annualized, up from roughly 2.7% just days earlier, driven by an unexpected plunge in the U.S. trade deficit and stronger consumer spending data. This dramatic jump reflects the trade gap narrowing to its lowest level since 2009, turning what had been a drag on growth into a significant contributor. While the GDPNow figure is a real-time nowcast rather than an official BEA release, it signals potentially robust economic momentum as we close out 2025 and reshapes market and policy expectations heading into 2026. Oil industry news – President Trump announced a US military action in Venezuela capturing and arresting President Nicolas Maduro over narcotic trafficking charges. This laid the groundwork for President Trump to announce that the US had control over Venezuelan oil and that US oil companies, who’s interests and investments in oil production was taken from them in 1976 when then President Carlos Andres Perez nationalized the oil industry, would be returned to US companies. Venezuela has the largest known oil reserves in the world. On Friday Trump hosted oil executives to formulate a plan to encourage investment to US oil companies into Venezuela promising security and cooperation from the Venezuelan government. The Dow Jones Industrial Average closed the week at 49,504.07 up 2.3% from 48,382.39 last week. It is already up 3% from 48,063.29 on December 31, 2025. The S&P 500 closed the week at 6,966.28, up 1.6% from 6,858.47 last week. The S&P is up 1.8% from 6,845.50 on December 31, 2025. The Nasdaq closed the week at 23,702.88, up 2% from 23,235.63 last week. It is up % from 23,241.99 on December 31, 2025. The 10-year treasury bond closed the week yielding 4.18%, almost unchanged from 4.19% last week. The 30-year treasury bond yield ended the week at 4.82%, down from 4.86% last week. We watch bond yields because mortgage rates follow bond yields. Have a Great Weekend! |

News & Media