The real estate market has remained very active. We are continuing to see sales at a solid pace-certainly much stronger than what we experienced in the second half of 2025. The year started off with good momentum and has stayed active despite rising interest rates. Mortgage rates are currently around 6⅜% for a 30-year fixed, which is down from where they were at the end of last week, when rates pushed well above 6.5% and even approached 6¾%. The Freddie Mac survey rates tend to lag a bit, but they reflect the same general trend.

Looking ahead, we’re set to receive key inflation data, including CPI and PCE. Inflation had been trending in the right direction, with CPI falling to 2.4% from a peak of 9.1% in 2022, which had investors optimistic and helped push mortgage rates below 6% earlier this year-the lowest levels since 2022. However, the recent conflict involving Iran has caused oil prices to spike from roughly $70 per barrel to around $110, leading to a noticeable increase in gas prices-about $1 per gallon nationwide. This introduces renewed inflationary pressure and is something the market will be watching closely.

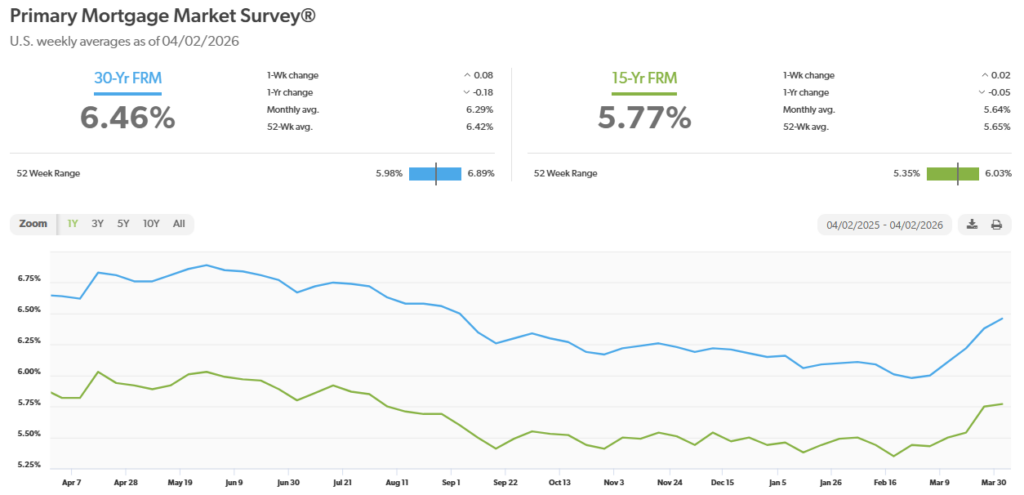

Mortgage rates – Every Thursday, Freddie Mac publishes interest rates based on a survey of mortgage lenders throughout the week. The Freddie Mac Primary Mortgage Survey reported that mortgage rates for the most popular loan products as of April 2, 2026, were as follows: The 30-year fixed mortgage rate was 6.46%, up from 6.38% last week. The 15-year fixed was 5.77%, up slightly from 5.75% last week.

The graph below shows the trajectory of mortgage rates over the past year.

U.S. Jobs Report – Hiring picked up in March – The Bureau of Labor and Statistics reported that 178,000 new jobs were created in March, far surpassing analyst’s expectation of 59,000 jobs. That was welcome news following a net loss of 133,000 in February. The unemployment rate ticked down to 4.3%, from 4.4% in February. Average hourly wages increased 0.2% month-over-month from February, and up 3.5% from one year ago. That marked the lowest year-over-year increase since 2021. Strong hiring is inflationary, but softer wages are deflationary, so the Fed will likely view this as neutral.

Stock markets – The Dow Jones Industrial Average closed the week at 45,504.67, up 0.7% from 45,166.64 last week. It is down 5.3% year-to-date from 48,063.29 on December 31, 2025. The S&P 500 closed the week at 6,582.69, up 3.4% from 6,368.85 last week. The S&P is down 3.8% year-to-date from 6,845.50 on December 31, 2025. The Nasdaq closed the week at 21,879.18, up 4.4% from 20,948.85 last week. It is down 5.9% year-to-date from 23,241.99 on December 31, 2025.

U.S. Treasury Bonds – The 10-year treasury bond closed the week yielding 4.35%, down from 4.44% last week. The 30-year treasury bond yield ended the week at 4.91%, down from 4.98% last week. We watch bond yields because mortgage rates follow bond yields.