| This week, markets continued their upward momentum, driven largely by strong corporate earnings, particularly from major tech companies, which helped push the S&P 500 and Nasdaq closer to recent highs. Positive earnings surprises reinforced confidence that corporate America remains resilient despite elevated interest rates. Economic data was mixed but generally supportive, with ongoing signs of steady consumer activity and a still-solid labor market. Treasury yields remained somewhat volatile but have stabilized off recent peaks, helping support equities. Ongoing geopolitical tensions remain a factor to watch, particularly for their potential impact on energy prices and inflation, but so far markets have largely absorbed the news without significant disruption. Overall, the tone of the market remains constructive, though investors continue to watch inflation trends and the Federal Reserve’s next moves closely as we head further into earnings season.

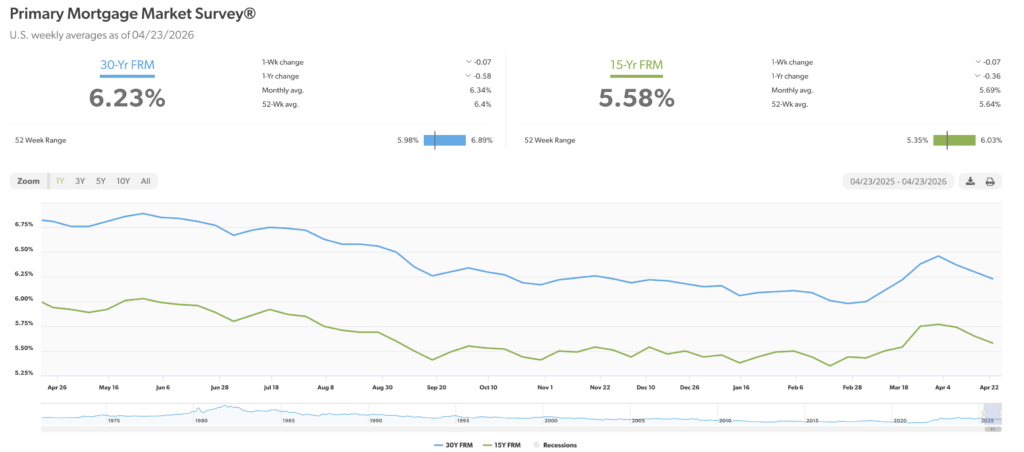

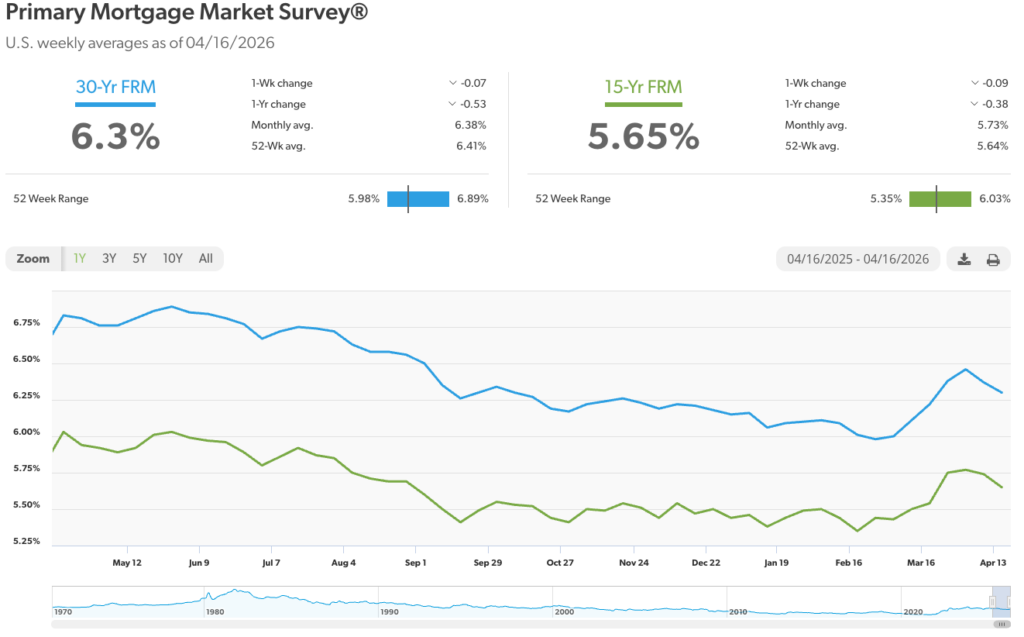

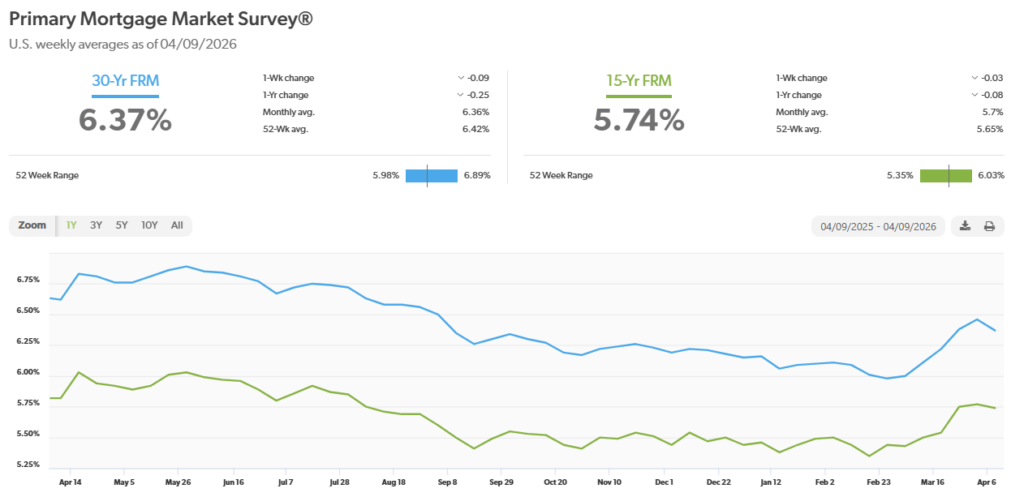

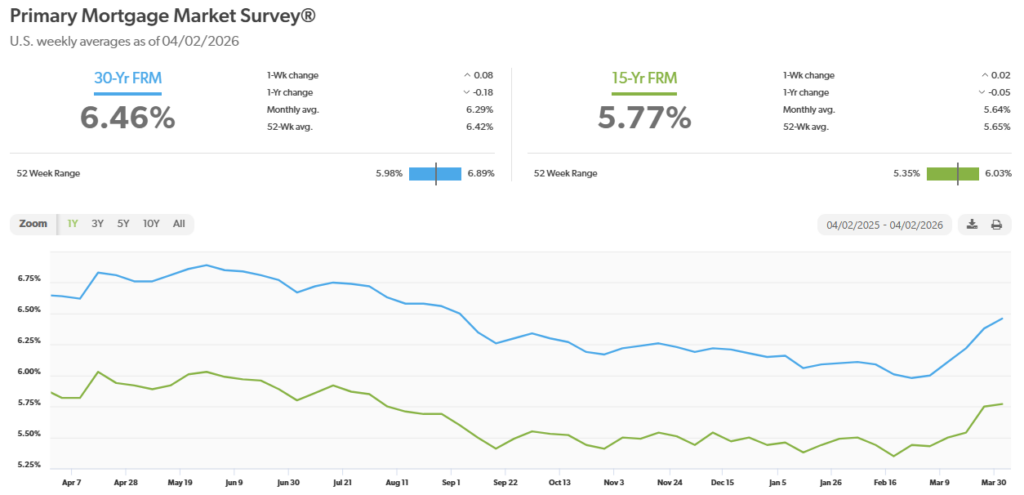

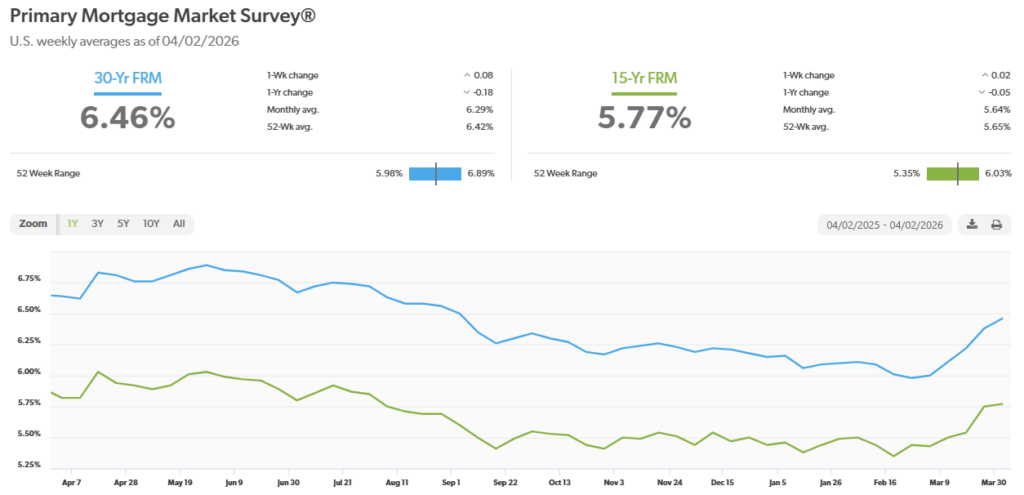

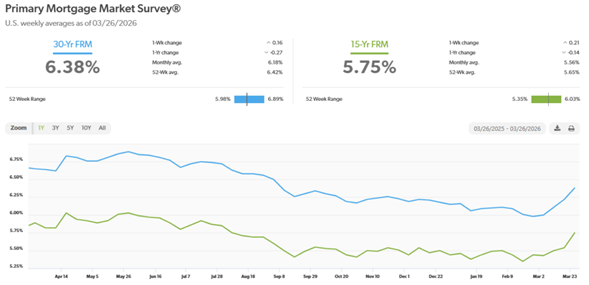

Mortgage rates – Every Thursday, Freddie Mac publishes interest rates based on a survey of mortgage lenders throughout the week. The Freddie Mac Primary Mortgage Survey reported that mortgage rates for the most popular loan products as of April 23, 2026, were as follows: The 30-year fixed mortgage rate was 6.23%, down from 6.3% last week. The 15-year fixed was 5.58%, down from 5.65% last week. The graph below shows the trajectory of mortgage rates over the past year. Stock markets – The Dow Jones Industrial Average closed the week at 49,223.80, down 0.5% from 49,447.43 last week. It is up 2.4% year-to-date from 48,063.29 on December 31, 2025. The S&P 500 closed the week at 7,164.83, up 0.5% from 7,126.06 last week. The S&P is up 4.7% year-to-date from 6,845.50 on December 31, 2025. The Nasdaq closed the week at 24,833.05, up 1.5% from 24,468.48 last week. It is up 6.8% year-to-date from 23,241.99 on December 31, 2025. U.S. Treasury Bonds – The 10-year treasury bond closed the week yielding 4.31%, up from 4.26% last week. The 30-year treasury bond yield ended the week at 4.91%, up from 4.88% last week. We watch bond yields because mortgage rates follow bond yields. Home sales are released on the third week of the month by the California Association of Realtors and the National Association of Realtors. Below is a summary of their reports. U.S. existing-home sales – March 2026 – The National Association of Realtors reported that existing-home sales totaled 3.98 million units on a seasonally adjusted annualized rate in March, down 3.6% from the number of homes sold in February. Year-over-year home sales were down 1% from the number of homes sold last March. The median price paid for a home in the U.S. in March was $408,800, up 1.4% year-over-year from $403,100 last March. California existing-home sales – The median price soared 7.1% in March as inventory tightened – The California Association of Realtors reported that existing-home sales totaled 265,320 on an adjusted annualized basis in March, down 3.5% from 274,820 annualized sales in February and down 2.5% from 272,020 last March. The statewide median price paid for a home was $889,190 in March, up 7.1% from $830,370 in February. Year-over-year March’s median price was up 0.4% from $885,900 one year ago. There were fewer listings in February. Housing inventory declined 17.5% month-over-month in March. The unsold inventory index dropped to a 3.3-month supply of homes for sale in March, down from 4-month in February.

Have a Great Weekend! |

Economic Update | Week Ending April 25, 2026