This week the stock market saw another week of positive territory with strong gains seen in all three indices as investors took into account bad weather as an excuse for some soft economic data. While U.S. export prices rose 0.2% in January, the third straight monthly increase, factory production fell 0.8% in January, the biggest drop in more than 4-1/2 years. The Dow closed out the week at 16,154.39 up 2.28% from last week’s close of 15,794.08. The Nasdaq was also up, ending the week at 4,244.03 up 2.86% from last week’s 4,125.86 close. The S&P 500 ended the week at 1,838.63, up 2.32% from last week’s 1,797.02 close.

This week the stock market saw another week of positive territory with strong gains seen in all three indices as investors took into account bad weather as an excuse for some soft economic data. While U.S. export prices rose 0.2% in January, the third straight monthly increase, factory production fell 0.8% in January, the biggest drop in more than 4-1/2 years. The Dow closed out the week at 16,154.39 up 2.28% from last week’s close of 15,794.08. The Nasdaq was also up, ending the week at 4,244.03 up 2.86% from last week’s 4,125.86 close. The S&P 500 ended the week at 1,838.63, up 2.32% from last week’s 1,797.02 close.

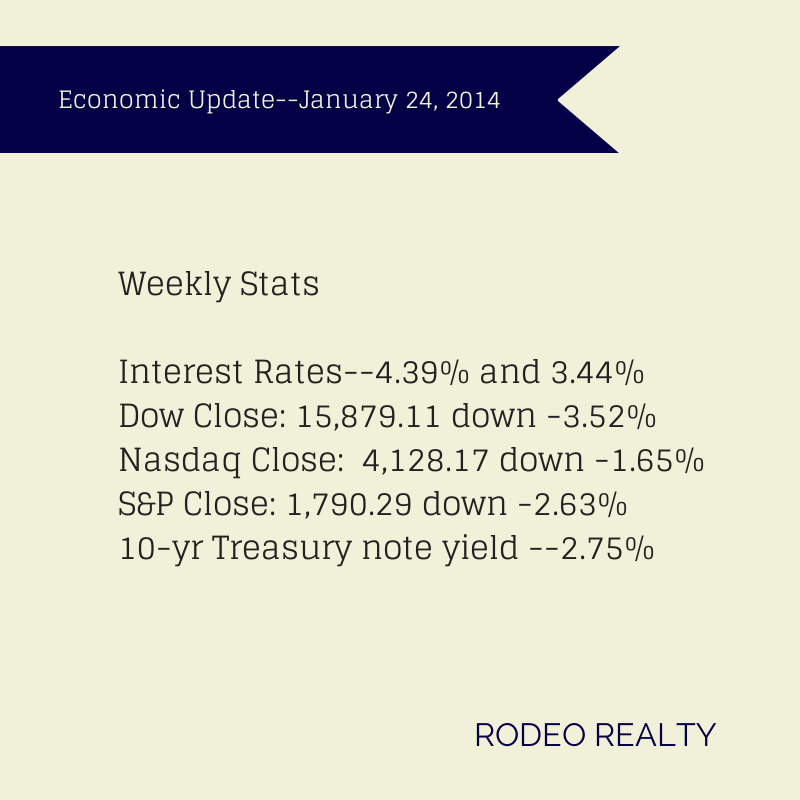

The 10-year Treasury note yield rate rose slightly to 2.75% after ending last week at 2.71%. It was 2.00% a year ago.

Interest rates saw a slight rise this week after several lower weeks. The Freddie Mac Weekly Primary Mortgage Market Survey showed that the 30-year-fixed rate up to 4.28% from 4.23% last week. The 15-year-fixed stayed solid at 3.33% the same as last week’s 3.33%. A year ago the 30-year fixed was at 3.53% and the 15-year was at 2.77%.

The latest quarterly report from the National Association of Realtors® shows that the

median existing single-family home price increased in 73% of measured markets, with 119 out of 164 metropolitan statistical areas (MSAs) showing gains based on closings in the fourth quarter compared with the fourth quarter of 2012. Forty-two areas, 26 % had double-digit increases. The national median existing single-family home price was $196,900 in the fourth quarter, up 10.1% from $178,900 in the fourth quarter of 2012. In the third quarter the median price rose 12.5% from a year earlier. In the West, existing-home sales dropped -12.7% in the fourth quarter, and are -8.1% below a year ago. Lack of inventory remains a concern. The median existing single-family home price in the West jumped 15.5% to $286,200 in the fourth quarter from the fourth quarter of 2012.

Credit reporting agency TransUnion released a report showing that the amount of late payments on home loans has hit the lowest level in more than 5 years. Nationwide, 3.85% of mortgage holders were at least two months behind on their payments in the October-December quarter, compared to 5.08% a year before.

The California Association of Realtors®reported that the percentage of home buyers who could afford to purchase a median-priced, existing single-family home in California in the fourth quarter of 2013 was unchanged from the third quarter of 2013 at 32%, but was down from 48% in fourth-quarter 2012, according to C.A.R.’s Traditional Housing Affordability Index (HAI). Home buyers needed to earn a minimum annual income of $89,240 to qualify for the purchase of a $431,510 statewide median-priced, existing single-family home in the fourth quarter of 2013.The median home price was $352,450 in fourth-quarter 2012, and an annual income of $66,860 was needed to purchase a home at that price. California housing affordability hit a record high of 56% in first quarter of 2012 but has steadily declined since then. In Los Angeles the affordability index in the fourth quarter of 2013 was 34%, down from the third quarter’s 35% and much reduced from the fourth quarter of 2012’s 50%.

DataQuick reported that home prices fell 3.8% in January compared with December and sales were down -9.9% year over year, though the median price was up 18.4% compared with January of last year. January’s median home price, $380,000, is the lowest since May 2013. For the six-county Southland area 14,471 new and resale homes and condos were sold last month, a three-year low for January. For Los Angeles alone, 5,308 homes were sold, a -7.4% decrease from January 2013. The median price however rose 20.6% from $340,000 to $410,000.

There was an article this week in the L.A. Times about home prices stalling. A broker was quoted in the Inland Empire. That is not what is happening here! I doubt it’s happening there either. We definitely need more homes on the market as we are seeing record sales prices! We all should have bought more Real Estate in the last few years. Let’s not be saying the same thing at years end!