By: Tim Logan

In more than two decades as a real estate agent, Marc Tahler has seen his client base of would-be buyers shift.

He used to see a lot of younger couples, married, maybe with a kid in tow or one on the way.

Lately, though, his buyers are trending a little older, and, kid or no, a lot fewer of them sport a wedding ring.

“I’m seeing more people who aren’t married,” said the agent with Rodeo Realty in Woodland Hills. “Sometimes, it’s a couple where both have been divorced, buying as partners. Or one buys and the other puts some money in. It’s all becoming more common.”

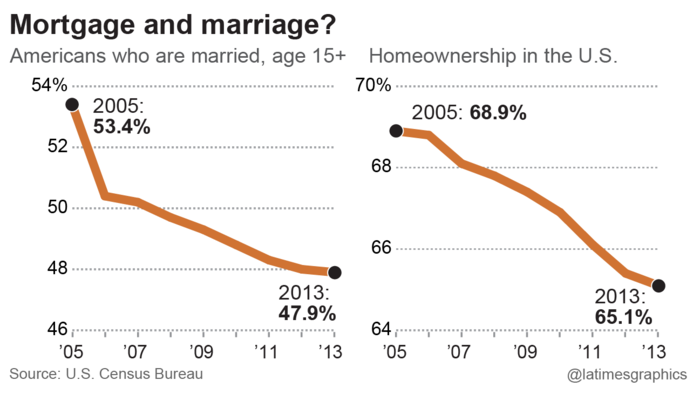

A generation of young people who are getting married later — or not at all — are also taking a different approach to one of the biggest financial decisions most of them will ever make. They no longer see marriage as a prerequisite to a mortgage.

Is there a correlation?

“These key life-stage things impact when we buy, what we buy and where we buy,” said Mollie Carmichael, a principal at John Burns Real Estate Consulting in Irvine. “But … young people today aren’t living by the same rules as 20 or 30 years ago.”

Unmarried couples, same-sex partners, even pairs of roommates going halvesies make up a much bigger chunk of the housing market than they did a generation ago, said Rachel Drew, a researcher at Harvard University’s Joint Center for Housing Studies.

“The decline in married couples, among younger buyers, is almost entirely offset by growth in unmarried couples. You’re not actually seeing a decline in two-adult households,” she said. “[Unmarried couples] are much more likely than a single person to buy a home. They’re acting like married couples.”

That’s what Krystle Mangaccat is doing. She and her boyfriend closed this week on a house in Northridge, a single-family home with three bedrooms, 2 1/2 baths and plenty of room for their dogs — and maybe someday their kids.

They’re not married yet, but after four apartments in three years, they were ready to settle in a place of their own, Mangaccat said. And, she said, the choice between using their savings on a down payment or a wedding was kind of a no-brainer.

“We’re practical people,” she said. “A house is a long-term thing. We’d rather spend our money on that than on throwing a big party.”

That’s a choice more couples are making lately, according to a study last year by real estate website Redfin, which notes that the average wedding and honeymoon costs about $35,000, enough for a down payment for many home buyers.

Other would-be house hunters plan to buy regardless of their marital status, like Yvonne Carrasco. The 33-year-old public relations professional has been saving up a down payment for years now. She figures she’s a year or so away, and hopes to buy something in 2016.

These key life-stage things impact when we buy, what we buy and where we buy. But … young people today aren’t living by the same rules as 20 or 30 years ago.

– Mollie Carmichael, a principal at John Burns Real Estate Consulting in Irvine

A house will be something of her own that she could bring to a marriage someday, or an asset for herself.

“I think a lot of people my age have come to the realization that marriage is almost like a bonus. If it happens, great. If it doesn’t, great,” she said. “But it’s important to put yourself in the situation to feel safe and secure.”

And for some, the outlook is that homeownership remains a long way off, marriage aside.

Carlos Garcia is a 31-year-old law student at Santa Clara University. He and his girlfriend are thinking about whether to move back to their native Southern California or stay in the Bay Area after they graduate in 2016.

Either way, Garcia notes, they’re looking at “literally the two most expensive parts of the country.”

With six-figure law school debt and sky-high home prices, he worries that even two attorneys’ salaries may not qualify them for a mortgage in a neighborhood where they want to live.

“I really have no reasonable aspirations of being able to buy a house for probably 10 years,” Garcia said. “It’s disheartening.”

Whatever the reason — fewer marriages or more challenging finances — younger buyers are waiting longer to buy homes. That helped slow the housing market in 2014.

In Southern California, the number of homes sold through November was down 9.8% for the year, to its lowest level since 2011, and well below long-term averages. That’s despite near-record-low interest rates and an improving economy.

Though unmarried couples may be more willing to buy houses together, some still see a marriage as a key driver of homeownership.

“It’s a pretty straightforward link,” said Richard Green, director of USC’s Lusk Center for Real Estate. “Married people buy houses. Single people rent.”

New home loan helps lower-income borrowers build equity quickly

New home loan helps lower-income borrowers build equity quickly

Just 48.7% of California households were headed by married couples in 2013, according to Census Bureau figures, down from 51.1% in 2000, a difference of more than 300,000 households. And those married couples are far more likely to own their house — more than two-thirds do, compared with about 40% of non-married households.

That’s partly a matter of money, he notes. A married couple with two incomes is far better equipped to buy a home in Southern California at a time when the median-priced home in Los Angeles County costs nearly nine times what the average job pays in a year. Marriage makes the math work.

The math can work just as well for unmarried couples, but many continue to grapple with employment and income uncertainty, said Daniel Sanchez, a real estate agent with Partners Trust in Beverly Hills.

Sanchez works with a lot of 30-something buyers who are trying to sort out life changes, moves and jobs that they’re not so sure will last forever. They’re establishing careers later, getting married later, buying houses later.

“The dynamics have completely changed,” said Sanchez, who at 35 is himself a renter and in “no rush” to buy. “Buying a home makes sense if you know you’re going to stay put, but we’re in a totally different time.”

For some, it makes sense whether they’re married or not — though negotiations over whether the house or the ring comes first can be tricky, real estate agent Tahler said.

He knows from personal experience, having just bought a house with his girlfriend of six years. They have a son together and wanted more space. But she hesitated.

“It became a little heated. She almost didn’t want to, specifically because we weren’t married,” Tahler said. “She settled — for the moment. She’s still pushing the marriage, though.”